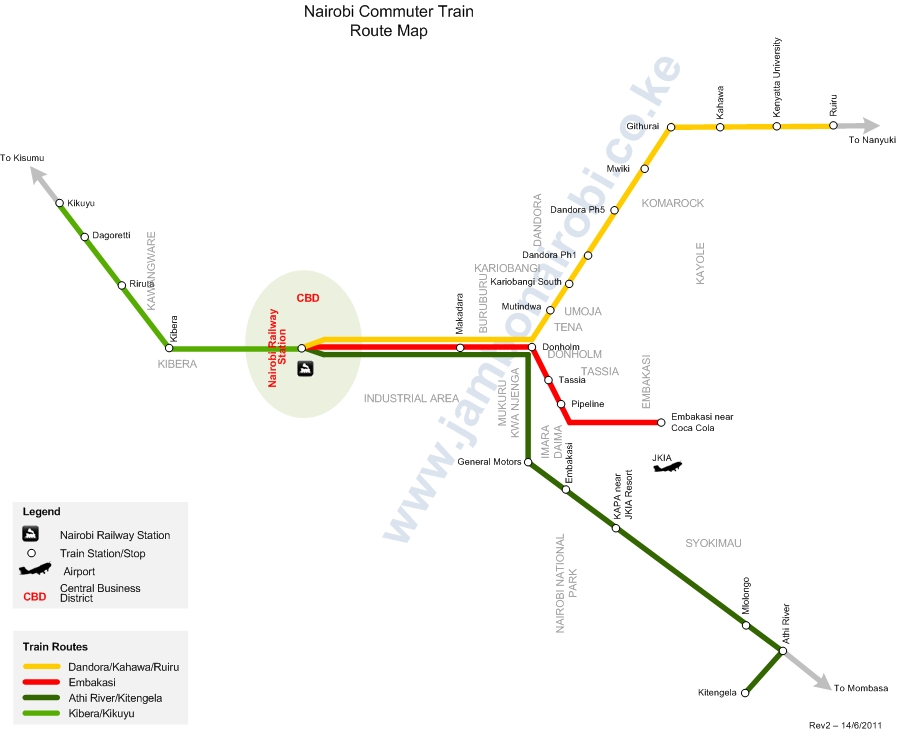

It is gratifying to see the commuter railway system being built. http://www.businessdailyafrica.com/Corporate+News/Future+of+Nairobis+transport+takes+shape+/-/539550/1416372/-/157kn4w/-/index.html

At the moment the only line is the 2.2kms from Syokimau to Embakasi but I hope the process/construction is fast-tracked from CBD (Moi Ave) to JKIA which will cut down on the traffic plying the roads between the CBD & JKIA.

A conceptual sketch of the Commuter Railway System

Tuesday, May 29, 2012

{kind=link}

Kenya Airways Rights Issue Results Announcement Delayed

The date of the announcement of the of the results of KQ's 2012 Rights Issue has been pushed from 30th May 2012 to 6th June 2012.

I wonder why...

I wonder why...

Sunday, May 27, 2012

Kenya will remain King of the East African jungle

I came across this little tidbit in The East African... Museveni backs First Lady for the presidency

This is not unique to Uganda.

- USA - Bill Clinton who backed his wife, Hillary Clinton, for the top job in 2008 though this was 8 years AFTER he retired as the president.

- Argentina - Cristina Elisabet Fernández de Kirchner succeeded her husband as the president in 2007

- India - Rajiv Gandhi succeeded his mother, Indira Gandhi, as PM after she was assassinated in 1984

Unfortunately for Uganda, the tension & potential instability over the Yoweri Museveni succession will allow Kenya to steal a march over Uganda in the following areas:

- Infrastructure - Railway, Roads & Air. It's simple. Kenya plans to build a railway from Mombasa/Lamu to South Sudan. The earlier plan was to extend the Mombasa-Nairobi-Kampala line to Hoima-Juba but now it is likely Kenya might just go Lamu-Juba (with a spur to Ethiopia). The loss to Uganda will be substantial. Add roads by-passing Uganda heading to South Sudan. As for Air Travel, Kenya is far ahead already & a new/expanded airport will only help extend the lead.

- Oil Refinery - Uganda is slightly ahead on this matter since it found viable oil finds 3 years prior to Kenya (2012). The good news for Kenya is that South Sudan (as well as potential oil finds in Kenya) makes for a better case for a new refinery planned for Lamu.

Kenya's only competitor for good governance (not that the bar is high) is Rwanda which plans to build a new airport in Kigali to compete as an East African hub. Rwanda has been in the forefront of integration & plans to sue other EAC countries to reduce non-tariff barriers.

It is unfortunate that Kenya will benefit at the expense of the regional neighbours but this is not Kenya's doing. Ideally, there should be a concerted effort to increase regional trade by reducing barriers but investing in unstable situations is pricier & not every investor is comfortable.

Kenya screwed up in 2007-8. It is easy to blame the politicians but they did not go out with machetes to hack their neighbours but idiots/sadists among us did. Kenya is an African country & I (sadly) expect at a few election related deaths. Not unique to Kenya or Africa. This happens regularly in Pakistan, Middle East (Bahrain, Iraq, etc), India, etc.

*Yes, I am being (slightly) pessimistic but very few regime changes or elections in Africa over the past 10 years have been violence free. Perhaps these were not at the scale of the Kenyan debacle but somewhat violent*

Tanzania (generally peaceful political transitions) with it's misguided "We are Southern Africans" has held it back from usurping Kenya's clout. I expect the economy of Northern Tanzania to remain reliant on Kenya - a net consumer of fruits, vegetables & grains. If Kenya expands the Port of Mombasa before the Tanzanians smell the roses, then the supply of many goods into Tanzania will be dominated by supply chains via Kenya.

*** As an aside, thumbs up to Kiran Jain (born in Kibos, Kisumu & whose parents still live here) who heads Dehli Airport's "airline marketing & route development". Hopefully, she returns to Kenya at some point & revamps JKIA!!!

Thursday, May 24, 2012

Corporate Governance & Independent Directors

Warren Buffet in his Letter to Shareholders in the 2006 Berkshire Annual Report

In selecting a new director, we were guided by our long-standing criteria, which are that board

members be owner-oriented, business-savvy, interested and truly independent. I say “truly” because many directors who are now deemed independent by various authorities and observers are far from that, relying heavily as they do on directors’ fees to maintain their standard of living. These payments, which come in many forms, often range between $150,000 and $250,000 annually, compensation that may approach or even exceed all other income of the “independent” director. And – surprise, surprise – director compensation has soared in recent years, pushed up by recommendations from corporate America’s favorite consultant, Ratchet, Ratchet and Bingo. (The name may be phony, but the action it conveys is not.) Charlie and I believe our four criteria are essential if directors are to do their job – which, by law, is to faithfully represent owners. Yet these criteria are usually ignored. Instead, consultants and CEOs seeking board candidates will often say, “We’re looking for a woman,” or “a Hispanic,” or “someone from abroad,” or what have you. It sometimes sounds as if the mission is to stock Noah’s ark. Over the years I’ve been queried many times about potential directors and have yet to hear anyone ask, “Does he think like an intelligent owner?”

The questions I instead get would sound ridiculous to someone seeking candidates for, say, a

football team, or an arbitration panel or a military command. In those cases, the selectors would look for

people who had the specific talents and attitudes that were required for a specialized job. At Berkshire, we are in the specialized activity of running a business well, and therefore we seek business judgment.

When I criticized the Board of Kenya Airways for not looking out for Shareholder Interests, I had in mind what Warren Buffett has said over the years.

1) Directors should have a significant stake in the business. The best Non-Executive directors, who watch over the CEO & Senior Management have have to have skin in the game, hence open to losses/downside, not pandering to the CEO or Senior Management to receive hefty perks, with all upside & no downside.

KQ's Board [excludes the corporate directors representing KLM & GoK] have less than 25,000 shares worth less than 400,000/- whereas the perks/compensation (as reported) were about KES 6mn. I doubt we even know the full value of the free non-work related flights they (& their families) received thanks to KQ.

2) Directors have to have business judgement not political appointees or because they are 'nice' people.

So many examples of directors who should not be on many boards. Look at the appointees/nominees on GoK controlled (or influenced) firms like Kenya Airways, EA Portland Cement, National Bank of Kenya, etc. Compare the performance of these firms vs their peers or even the NSE in general.

3) Directors should be compensated by having 'locked-in' shares or options not just cash compensation.

KenolKobil's CEO has options (amounting to at least 4% of the outstanding shares) which has translated into superb growth in earnings as well as an on-going Takeover Bid. Kestrel Capital expects a (at least) 20/- buyout offer which is 60% above the last traded price & significantly higher than the NAV/share. Compare to what the Board of Directors of KQ did to its existing shareholders.

In selecting a new director, we were guided by our long-standing criteria, which are that board

members be owner-oriented, business-savvy, interested and truly independent. I say “truly” because many directors who are now deemed independent by various authorities and observers are far from that, relying heavily as they do on directors’ fees to maintain their standard of living. These payments, which come in many forms, often range between $150,000 and $250,000 annually, compensation that may approach or even exceed all other income of the “independent” director. And – surprise, surprise – director compensation has soared in recent years, pushed up by recommendations from corporate America’s favorite consultant, Ratchet, Ratchet and Bingo. (The name may be phony, but the action it conveys is not.) Charlie and I believe our four criteria are essential if directors are to do their job – which, by law, is to faithfully represent owners. Yet these criteria are usually ignored. Instead, consultants and CEOs seeking board candidates will often say, “We’re looking for a woman,” or “a Hispanic,” or “someone from abroad,” or what have you. It sometimes sounds as if the mission is to stock Noah’s ark. Over the years I’ve been queried many times about potential directors and have yet to hear anyone ask, “Does he think like an intelligent owner?”

The questions I instead get would sound ridiculous to someone seeking candidates for, say, a

football team, or an arbitration panel or a military command. In those cases, the selectors would look for

people who had the specific talents and attitudes that were required for a specialized job. At Berkshire, we are in the specialized activity of running a business well, and therefore we seek business judgment.

When I criticized the Board of Kenya Airways for not looking out for Shareholder Interests, I had in mind what Warren Buffett has said over the years.

1) Directors should have a significant stake in the business. The best Non-Executive directors, who watch over the CEO & Senior Management have have to have skin in the game, hence open to losses/downside, not pandering to the CEO or Senior Management to receive hefty perks, with all upside & no downside.

KQ's Board [excludes the corporate directors representing KLM & GoK] have less than 25,000 shares worth less than 400,000/- whereas the perks/compensation (as reported) were about KES 6mn. I doubt we even know the full value of the free non-work related flights they (& their families) received thanks to KQ.

2) Directors have to have business judgement not political appointees or because they are 'nice' people.

So many examples of directors who should not be on many boards. Look at the appointees/nominees on GoK controlled (or influenced) firms like Kenya Airways, EA Portland Cement, National Bank of Kenya, etc. Compare the performance of these firms vs their peers or even the NSE in general.

- KQ has destroyed shareholder value. The recent Rights Offer (16:5) was at 67% discount to NAV.

- EAPCC vs Bamburi vs Athi River Mining. ARM (the CEO has a significant stake) has created significant shareholder wealth.

- NBK vs Equity vs NIC vs Diamond vs I&M Bank. NBK has stagnated (I remain an admirer of the CEO) while the others grew tremendously. Equity and I&M Bank's CEOs have significant stakes in the bank. The directors of Diamond Trust & NIC represent the majority/key shareholders.

3) Directors should be compensated by having 'locked-in' shares or options not just cash compensation.

KenolKobil's CEO has options (amounting to at least 4% of the outstanding shares) which has translated into superb growth in earnings as well as an on-going Takeover Bid. Kestrel Capital expects a (at least) 20/- buyout offer which is 60% above the last traded price & significantly higher than the NAV/share. Compare to what the Board of Directors of KQ did to its existing shareholders.

Wednesday, May 23, 2012

Investment Bankers - Untrustworthy. Ask Warren Buffett

Warren Buffett: “Don’t ask the barber whether you need a haircut.”

Warren Buffett does not trust Investment Bankers. I am not surprised. One of the world's savviest investor has a low opinion of Investment Bankers. So should we.

We have see what they did to investors, shareholders & the public during the housing crisis among other debacles.

http://www.guardian.co.uk/technology/2012/may/23/facebook-founder-regulators-lawsuits?CMP=twt_fd&CMP=SOCxx212

The article (courtesy The Guardian) has this to say:

Goldman Sachs decided to sell nearly half its holding, while Manhattan hedge fund Tiger Global increased its sell-off from 3m to 23m shares. Those most likely to have seen the analysts' forecasts may have decided that the shares were unlikely to enjoy the customary day-one surge, seen when Google and the professional networking site LinkedIn went public. Basically, for those in the know, at $38 a share Facebook was a "sell".

As you can see GS decided to sell out while probably encouraging their clients to buy!

Of course, investor who bought at $38 or higher are to blame as well. The ratios were outrageously high.

In Kenya, we have the case of SIB benefitting from a less than savoury deal on the Kenya Airways Rights Issue. Here is some interesting reading!

The Flying Rip-off

The late to the party Parliament to probe KQ Rights Issue

As outlined in this article, the perverse incentives for SIB to make sure the Rights Issue went through even if the deal hurt existing shareholders. The Board of Directors failed in it's duty to protect existing shareholders.

If I had to replace the entire Board of Directors of KQ with Warren Buffett, I would do it in a fraction of a heartbeat.

Warren Buffett does not trust Investment Bankers. I am not surprised. One of the world's savviest investor has a low opinion of Investment Bankers. So should we.

We have see what they did to investors, shareholders & the public during the housing crisis among other debacles.

http://www.guardian.co.uk/technology/2012/may/23/facebook-founder-regulators-lawsuits?CMP=twt_fd&CMP=SOCxx212

The article (courtesy The Guardian) has this to say:

Goldman Sachs decided to sell nearly half its holding, while Manhattan hedge fund Tiger Global increased its sell-off from 3m to 23m shares. Those most likely to have seen the analysts' forecasts may have decided that the shares were unlikely to enjoy the customary day-one surge, seen when Google and the professional networking site LinkedIn went public. Basically, for those in the know, at $38 a share Facebook was a "sell".

As you can see GS decided to sell out while probably encouraging their clients to buy!

Of course, investor who bought at $38 or higher are to blame as well. The ratios were outrageously high.

In Kenya, we have the case of SIB benefitting from a less than savoury deal on the Kenya Airways Rights Issue. Here is some interesting reading!

The Flying Rip-off

Kenya Airways - Commissions Payment Scam

The late to the party Parliament to probe KQ Rights Issue

As outlined in this article, the perverse incentives for SIB to make sure the Rights Issue went through even if the deal hurt existing shareholders. The Board of Directors failed in it's duty to protect existing shareholders.

If I had to replace the entire Board of Directors of KQ with Warren Buffett, I would do it in a fraction of a heartbeat.

Sunday, May 20, 2012

CEOs buying Shares in their firms

Well, hats off to Martin Oduor-Otieno who now has shares in KCB.

Adan Mohamed also bought some shares in BBK.

It is not clear if these shares have been purchased directly or via an ESOP.

http://www.businessdailyafrica.com/Corporate+News/KCB+Barclays+chiefs+buy+shares+in+their+banks+/-/539550/1409828/-/a2cxe5z/-/index.html

Mr Mohammed bought 296, 000 currently worth Sh4 million while Mr Oduor-Otieno acquired 509,180 shares now valued at Sh12 million —making them top shareholders among the lenders’ directors and executives and an entry on the investor registry.

Readers may recall my disgust at the actions of the Board of Directors of Kenya Airways who shamelessly approved a Rights Issue at KES 14 when the NAV of each KQ share was 50/- (per the latest audited Financial Statements).

I compared the performance of firms like Equity Bank, Athi River Mining, ScanGroup and KenolKobil whose CEOs have a significant interest/shareholding in the firms they run versus Kenya Airways in which the CEO has ZERO shares!

Pradeep Paunrana of Athi River Mining announced the issuance of a Convertible Debt instrument that would help ARM grow WITHOUT destroying value for existing shareholders. That's the type of CEO a firm needs. One who cares about shareholders, not just his salary, bonuses, perks & benefits but feels no pain when shareholder lose.

I would encourage that MOO prudently buys more shares in KCB throughout the year which will give other shareholders faith that they sink or swim together. I would like to point out that Sunil Narshi Shah (a former, now retired, director) owned 5% of KCB at one point. He would keep an eye on the happenings in KCB since his 'wealth' was directly affected by the going on at the top.

Adan Mohamed also bought some shares in BBK.

It is not clear if these shares have been purchased directly or via an ESOP.

http://www.businessdailyafrica.com/Corporate+News/KCB+Barclays+chiefs+buy+shares+in+their+banks+/-/539550/1409828/-/a2cxe5z/-/index.html

Mr Mohammed bought 296, 000 currently worth Sh4 million while Mr Oduor-Otieno acquired 509,180 shares now valued at Sh12 million —making them top shareholders among the lenders’ directors and executives and an entry on the investor registry.

Readers may recall my disgust at the actions of the Board of Directors of Kenya Airways who shamelessly approved a Rights Issue at KES 14 when the NAV of each KQ share was 50/- (per the latest audited Financial Statements).

I compared the performance of firms like Equity Bank, Athi River Mining, ScanGroup and KenolKobil whose CEOs have a significant interest/shareholding in the firms they run versus Kenya Airways in which the CEO has ZERO shares!

Pradeep Paunrana of Athi River Mining announced the issuance of a Convertible Debt instrument that would help ARM grow WITHOUT destroying value for existing shareholders. That's the type of CEO a firm needs. One who cares about shareholders, not just his salary, bonuses, perks & benefits but feels no pain when shareholder lose.

I would encourage that MOO prudently buys more shares in KCB throughout the year which will give other shareholders faith that they sink or swim together. I would like to point out that Sunil Narshi Shah (a former, now retired, director) owned 5% of KCB at one point. He would keep an eye on the happenings in KCB since his 'wealth' was directly affected by the going on at the top.

Friday, May 18, 2012

Parliament to probe KQ Rights Issue

Via Daily Nation Page 6 of 18th May 2012 (I do not have a link)

A parliamentary investigation has been ordered into the justconcluded Kenya Airways rights issue after questions were raised on the process.

Below is the blogpost I had posted earlier in April 2012.

KQ Rights Issue Commission Scam

A parliamentary investigation has been ordered into the justconcluded Kenya Airways rights issue after questions were raised on the process.

Deputy Speaker Farah Maalim referred the matter to the parliamentary Finance committee yesterday after a member questioned how a stockbroker was picked and paid Sh100 million.

KQ plans to raise Sh2.7 billion for expansion and acquisition of additional aircraft in the rights issue which was launched by President Kibaki in March.

The government holds 23 per cent of KQ’s total issued capital.

Yesterday, Igembe North MP Ntoitha M’Mithiaru questioned the procedure of selecting stockbrokers for the submission of the provisional allotment letter and whether the service attracted a commission.

He also questioned whether the submission of the provisional allotment letter was a separate service from the advisory services provided by transaction adviser.

The transaction adviser in the rights issue was CFC Stanbic Bank Limited with CFC Stanbic Financial Services Limited as the lead transaction stockbroker. Standard Investment Bank Ltd was the lead sponsoring stockbroker.

Finance assistant minister Dr Oburu Odinga said the mandate for submission of the provisional allotment letter was with the lead sponsoring brokers who were competitively appointed by KQ.

Mr Maalim directed the Finance committee to report back to the House in a week’s time.

Sh100m Millions of shillings stockbroker was paid by Kenya Airways.Below is the blogpost I had posted earlier in April 2012.

KQ Rights Issue Commission Scam

Tuesday, May 15, 2012

KenolKobil Takeover - Could Puma list on the NSE

This is an interesting article from the FT published in Sep 2011.

http://www.ft.com/cms/s/0/14f9a590-ea80-11e0-b0f5-00144feab49a.html#ixzz1uxUpVLfx

The trader on Thursday said it has sold a 20 per cent stake in Puma Energy, its petroleum terminals and storage business, to Sonangol Holdings, a subsidiary of Angola’s state-owned oil company. The parties did not disclose financial details.

“The sale is a step to prepare the company for a listing in the future,” Pierre Eladari, Puma Energy’s chief executive, told the Financial Times in an interview.

It seems that Puma may have an incentive to do the following:

http://www.ft.com/cms/s/0/14f9a590-ea80-11e0-b0f5-00144feab49a.html#ixzz1uxUpVLfx

The trader on Thursday said it has sold a 20 per cent stake in Puma Energy, its petroleum terminals and storage business, to Sonangol Holdings, a subsidiary of Angola’s state-owned oil company. The parties did not disclose financial details.

“The sale is a step to prepare the company for a listing in the future,” Pierre Eladari, Puma Energy’s chief executive, told the Financial Times in an interview.

It seems that Puma may have an incentive to do the following:

- Puma makes an Offer to swap KK shares for Puma shares in the future.

- Keep the listing 'live' [even if suspended] in Kenya until the Puma IPO is complete.

- The KK shares are then 'converted' to Puma shares and trade on the NSE [as well as being fungible & traded on other exchanges e.g. Angola [when it finally goes live], in Asia [HK or Singapore] or London.

Puma Energy has not completed a Takeover/Buyout of Minority S/holders of (former) BP Zambia for almost 2 years. Is the final endgame a cross-listing of Puma shares in multiple countries?

Puma/KK does business in the following countries with Stock Exchanges:

- Kenya (KK's Primary Listing)

- Tanzania

- Uganda

- Rwanda

- Zambia (Puma Energy Zambia's Primary Listing)

- Botswana

If Puma Energy offers KK's shareholders the option of swapping into Puma's shares, it might soothe a few nerves since not all minority shareholders (or so it seems) want out of KK. Some shareholders are very protective of & loyal to KK as well.

Friday, May 11, 2012

KenolKobil (Takeover) - Update

The shares of KK have been indefinitely suspended from trading by the CMA starting 8th May 2012, following the Cautionary Statement released on 7th May 2012.

See Link to Prior Blogpost - with link to Cautionary Statement

It is not clear if the CMA issued the suspension notice based on KK's request or acted unilaterally. There has been a lot of debate of the appropriateness or justification of the suspension since some shareholders cannot exit their positions. This reminds me of the (failed) BOC takeover bid of Carbacid when the shares of both firms were suspended from trading for 4 years from 2005 to 4th Nov 2009.

The management of KK feels that the Takeover (at least the sale of shares in KK to Puma Energy) will be completed in 2012 which would leave the Minority Shareholders in the cold.

The CMA has to protect the Minority Shareholders by ensuring they are given the right to offer their shares to Puma at a similar price (or value) to Puma as the Key Shareholders. There will be the question about KK remaining a Listed Firm but based on what Puma's actions in Zambia, it seems unlikely if Puma can get 80% of the shares offered to them.

In Zambia, Puma purchased BP's shares in BP Zambia (renamed Puma Zambia) then ran into some headwind. I am not sure of the full details but it seems Puma will make a Takeover offer for the remainder it does not own. Due to lack of Listings in Zambia, the LuSE & SEC seemed reluctant to let Puma Zambia de-list. Furthermore, the price on LuSE has tripled since the sale by BP to Puma so Puma may not have an incentive to pay the market price.

*The LuSE & SEC have also blocked Airtel from delisting Celtel Zambia (in which it bought a majority stake from Celtel International) by buying out Minority Shareholders then de-listing. The shares have been suspended from trading indefinitely as well!

In essence, will Puma pay for 25% (Minority Shareholders) today for what it paid for the 75% (BP's shares) 3 years ago? I don't have all the details but this should be interesting & will it apply to the Kenyan situation?

A high enough price offered by Puma would convince most Minority Shareholders to sell their shares. The ranges vary but Kestrel Capital (a far better outfit than the Not-The-Standard Investicon Skank) who are also acting as advisers to the Key Shareholders did indicate a value of KES 17.25 in their last research report.

My valuation is higher:

See Link to Prior Blogpost - with link to Cautionary Statement

It is not clear if the CMA issued the suspension notice based on KK's request or acted unilaterally. There has been a lot of debate of the appropriateness or justification of the suspension since some shareholders cannot exit their positions. This reminds me of the (failed) BOC takeover bid of Carbacid when the shares of both firms were suspended from trading for 4 years from 2005 to 4th Nov 2009.

The management of KK feels that the Takeover (at least the sale of shares in KK to Puma Energy) will be completed in 2012 which would leave the Minority Shareholders in the cold.

The CMA has to protect the Minority Shareholders by ensuring they are given the right to offer their shares to Puma at a similar price (or value) to Puma as the Key Shareholders. There will be the question about KK remaining a Listed Firm but based on what Puma's actions in Zambia, it seems unlikely if Puma can get 80% of the shares offered to them.

In Zambia, Puma purchased BP's shares in BP Zambia (renamed Puma Zambia) then ran into some headwind. I am not sure of the full details but it seems Puma will make a Takeover offer for the remainder it does not own. Due to lack of Listings in Zambia, the LuSE & SEC seemed reluctant to let Puma Zambia de-list. Furthermore, the price on LuSE has tripled since the sale by BP to Puma so Puma may not have an incentive to pay the market price.

*The LuSE & SEC have also blocked Airtel from delisting Celtel Zambia (in which it bought a majority stake from Celtel International) by buying out Minority Shareholders then de-listing. The shares have been suspended from trading indefinitely as well!

In essence, will Puma pay for 25% (Minority Shareholders) today for what it paid for the 75% (BP's shares) 3 years ago? I don't have all the details but this should be interesting & will it apply to the Kenyan situation?

A high enough price offered by Puma would convince most Minority Shareholders to sell their shares. The ranges vary but Kestrel Capital (a far better outfit than the Not-The-Standard Investicon Skank) who are also acting as advisers to the Key Shareholders did indicate a value of KES 17.25 in their last research report.

My valuation is higher:

- The lawsuit vs KPC. I did not understand why the judges thought the award was too high in view of the 'economy' when the various scams KPC has indulged in are of similar, if not higher, amounts! I will reserve my judgement on their judgement. At a gross value of KES 6bn that is 4/- PBT (2.75 PAT) added to NAV. Of course, it is speculative but KK, is not giving up & seems to have a good chance it will prevail.

- The Annual Report (Chairman's Statement & Comprehensive Income Statement) indicated a large potential loss in 1H 2012 due to Forward Forex Hedges. The net effect may be an EPS of 'zero' for 1H 2012 thus no net effect on valuation going forward.

- Huge real estate exposure in Kenya (especially in Nairobi & Central Province - whatever that is called nowadays) which has been Kenya's most productive areas. *There is even a place named after Kenol - Kenol Township (which I passed through) - near/towards Kangema!* KK has prime real estate for developmental purposes in Addis Ababa (Ethiopia) as well as Rwanda. It is very hard to estimate the gains in RE values but this could easily add KES 3-5 to the NAV as reported.

- The 2011 EPS was 2.21 (diluted). There will always be challenges for KK with the volatile KES, interest rates & oil prices but if that is a normalized EPS [a further discount required for ESOP, Management & CEO options] then using a PER of 10 [based on KK's consistent growth & current depressed market prices] this would be: 2.10 x 10 = 21/-

So if we add the 'business value' of 21/- (should be discounted by cheap/free rents on properties owned or long-term leased by KK) + (potential) award vs KPC + Development Real Estate (includes maximize use of current locations by adding stores, buildings, offices without closing the petrol stations) = 25/- less transaction expenses = 24/- net!

Thoughts?

Monday, May 07, 2012

KenolKobil vs Kenya Airways - Management Ownership

KenolKobil issued a "Cautionary Statement" - http://kenolkobil.com/index.php/component/content/article/58/311

As I have said before, there is a world of difference between firms like KK & KQ.

KK - The CEO among senior managers have shares & options in KK that take the share price & firms' performance into account.

KQ - The CEO has ZERO shares/options & the entire Board of Directors [excluding KLM & GoK as corporate directors] have less than 25,000 shares.

Now to excerpts from KK's announcement:

"the key shareholders of the Company signed an Exclusive Agreement with Puma Energy for the sale of their majority shareholdings in KenolKobil... and contemplates making a Take-Over offer to acquire all the shares in the Company..."

"The KenolKobil Board of Directors believes that this transaction... would be a very positive development for the KenolKobil Group... The contemplated transaction is in line with the already expressed wish of Management to drive the Group to new highs and the next level of business development..."

KK's shares traded at 12.55 - 12.70 on 7th May 2012. I expect the price to rise considerably as the key shareholders, BoD & Management [who care about all the Shareholders] have probably negotiated a price or deal that prices the shares at a price HIGHER than market price and closer, if not higher, than the Net Asset Value per Share.

Let's compare this to the BoD & Management of KQ who sold the Rights Issues shares at 14/- when the NAV was 50/- (2010-11 audited accounts). Of course, unlike the BoD/Management of KK, the folks at KQ are in it for the perks, free flights & huge allowances.

I had highlighted KenolKobil's Chairman & CEO (Jacob Segman) as someone with a vested interest in the firm he runs. This is unlike the Chairman, BoD & CEO of KQ who has ZERO shares thus had nothing to lose when the shares were sold in the Rights Issue at a 72% discount to NAV/Share.

Whereas it is not known what price the 'key shareholders' have agreed to sell their stake in KK at but it will most likely be at a significant premium to the price as of 7 May 2012.

And on a personal note, I am sure Not-The-Standard Investicon Skank is not advising KK...

*** Did you know Steve Jobs had a $1 salary from Apple? He was paid in Options.

And on a personal note, I am sure Not-The-Standard Investicon Skank is not advising KK...

*** Did you know Steve Jobs had a $1 salary from Apple? He was paid in Options.

Subscribe to:

Comments (Atom)